Bitcoin is the scarcest asset there is.

—Michael Saylor

In Goldman, Sachs We Trust

THE RECONDITE PROBLEMS of Federal Reserve policy were not the only questions that were agitating Wall Street intellectuals in the early months of 1929. There was worry that the country might be running out of common stocks. One reason prices of stocks were so high, it was explained, was that there weren't enough to go around, and, accordingly, they had acquired a "scarcity value." Some issues, it was said, were becoming so desirable that they would soon be taken out of the market and would not reappear at any price.

—JK Galbraith, The Great Crash of 1929, Chapter III

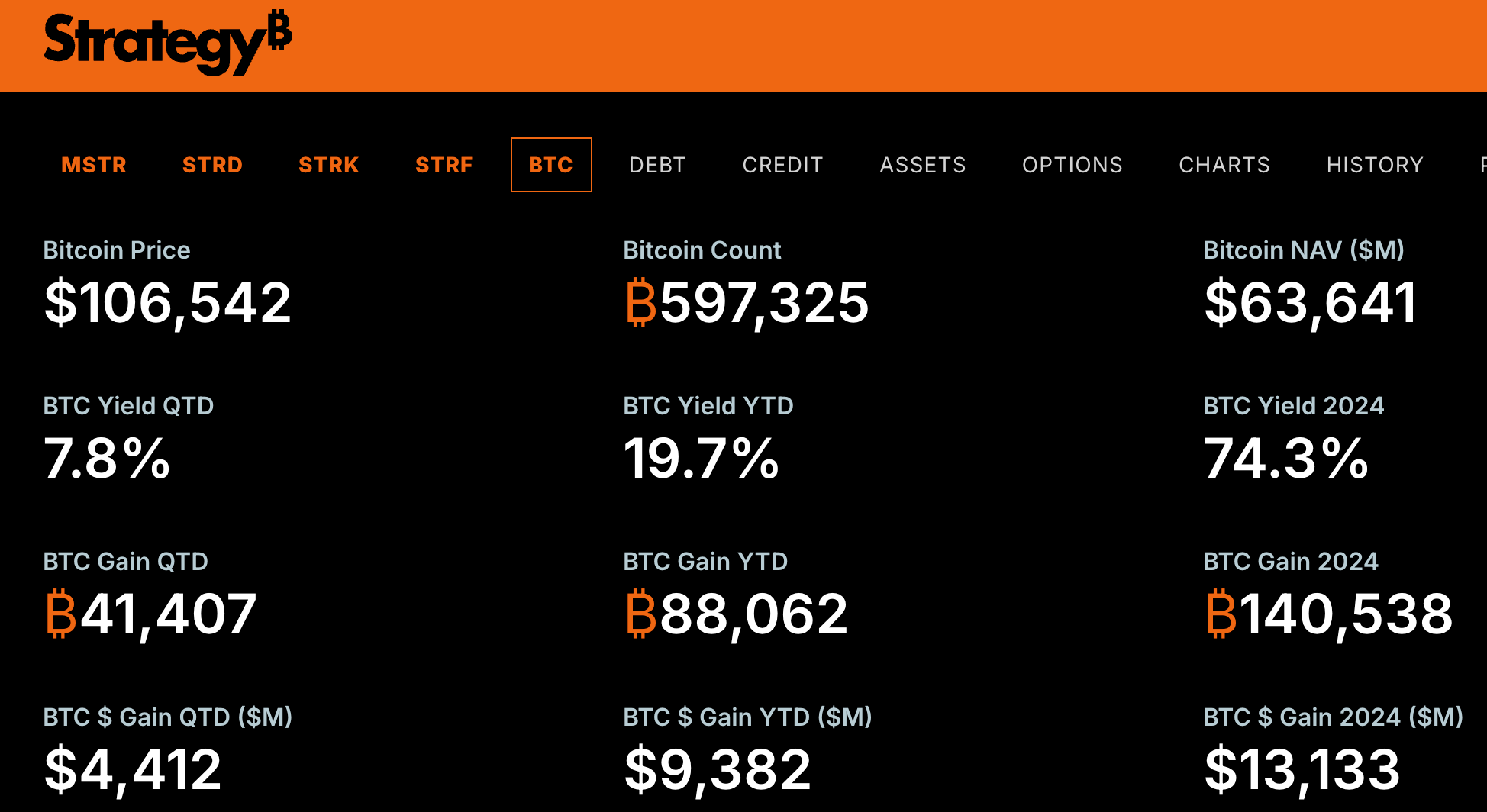

The Bitcoin Treasury craze is either genius or madness—and very possibly some combination of both. In Speculative Attack Part I, we explored how Michael Saylor’s MicroStrategy is weaponizing Wall Street's own financial engineering against the TradFi system by inverting the Symbolic Alchemy Of Risk; hundreds of companies now race to copy his playbook.

This is not the first time leveraged financial vehicles promised to democratize access to scarce assets using leverage and the accretive magic of mNAV premiums: the 1920s investment trust and holding bubble followed a similar script in the run-up to the 1929 Crash.

Receive our latest insights on X/Twitter @bewaterltd and visit our website bewaterltd.com

Not investment advice. For educational/informational purposes only. See Disclaimer.

Recent History: Greyscale Trust

Before exploring those century-old parallels, it's worth examining a more recent cautionary tale that directly involves Bitcoin itself. The Grayscale Bitcoin Trust was the conceptual predecessor to the Bitcoin treasury corporations, and its trajectory demonstrates how reliance on mNAV and leverage—even when the underlying Bitcoin and wrapper vehicle themselves remain unleveraged—can create systemic risks that ultimately destroy value for all participants.

Like Microstrategy more recently, Greyscale created a vehicle to “democratize” Bitcoin exposure through traditional securities markets—in this case a “pink sheet” OTC security—circumventing the operational complexities of Bitcoin self-custody. This innovation filled a genuine market need, as many individuals and institutions lacked either the infrastructure or regulatory ability to hold Bitcoin directly in their brokerage accounts; the SEC had not yet permitted Bitcoin ETFs on the market.

The Trust's success was reflected in its mNAV, which at times reached extraordinary levels of 2x or higher; investors were willing to pay double Bitcoin's price for the convenience of holding GBTC shares. This premium created what appeared to be a risk-free arbitrage opportunity: sophisticated investors could buy Bitcoin directly, contribute it to Grayscale’s trust, sell GBTC shares after a six-month lockup period, and profit from the mNAV premium upon sale.

While the Greyscale Trust itself held Bitcoin without any leverage—in other words, an even safer capital structure than MicroStrategy’s!—the broader ecosystem around it took on leverage. Hedge funds like Three Arrows (3AC) piled into the “Greyscale arbitrage trade” using significant leverage to maximize returns from this strategy. As Bitcoin's price declined in 2022 and the trust's mNAV premium evaporated, these leveraged positions became untenable.

3AC imploded in June 2022, setting off a crypto contagion leading to a “Crypto Winter”; forced liquidations and market panic accelerated the GBTC discount, which widened to historic lows. The discount remained stubbornly elevated until early 2024, when Greyscale was forced to convert the Trust into an ETF and allow daily redemptions at NAV (i.e., mNAV=1).

More History: Gold Trusts

Before Bitcoin was a glimmer in Satoshi’s eye—indeed, even before ETFs like GLD existed—gold trusts were the intellectual blueprint for Greyscale’s GBTC. In an era when investors sought exposure to physical gold—now known as “Bitcoin for Boomers”, but then widely regarded as the ultimate hedge against fiat currency debasement—options remained frustratingly limited.

The Spicer family built a remarkable business addressing this market need through their Central Fund of Canada (CEF) and Central GoldTrust; they generated profits by storing vaulted gold bullion for investors in an efficient, tax-advantaged structure through publicly listed closed end trusts. During a gold bull market, and with no liquid ETF alternative, investor demand for the trust often outpaced supply much as it did for Greyscale’s GBTC—causing the trusts to trade at a persistent premium to NAV in the early 2000s.

The Spicers enjoyed a position conceptually similar to Bitcoin treasury companies, whose mNAV premium now allows them to sell one dollar of Bitcoin for two dollars. When their trust's market value exceeded its NAV, they could issue new trust units at the inflated price, generating profit for the parent company (though unlike Bitcoin treasury companies, this value did not accrue to trust unitholders). Conversely, when the trust traded at a discount to its NAV, they could use the parent company's cash flows and savings to buy back trust units at the discounted price. This created a risk-free arbitrage opportunity that allowed the Spicers to capture the spread between the market price of the trust and its underlying gold value.

The landscape shifted dramatically after ETFs like GLD came to market in 2004. The advantage of closed-end trusts eroded in much the same way GBTC's did when Bitcoin ETFs received SEC approval. Gold trusts that had frequently traded at premiums to NAV began trading at persistent discounts to their NAV, creating significant unitholder dissatisfaction.

This vulnerability culminated in a historic hostile takeover by Sprott Inc. in 2015. Sprott merged the Spicer assets into what is now the Sprott Physical Gold Trust (PHYS), and later acquired the original Central Fund of Canada; they’ve subsequently introduced a physical uranium trust (SPUT) and a copper trust (COP). We’ll explore Sprott Inc. in greater detail in an upcoming series about the Multiflation Method.

Parallels To The 1920s Investment Trust Mania

"Progress is cumulative in science and engineering, but cyclical in finance."

—Jim Grant

Perhaps the most haunting precedent for the current Bitcoin TreasuryCo mania, however, comes from the 1920s. In The Great Crash 1929, JK Galbraith traced part of the Great Depression’s origins to the financial engineering innovations of the era: specifically, newly formed investment entities called “investment trusts” and “holding companies” that parallel Bitcoin treasury companies in many ways.

Investment Trusts

As Galbraith observed in his account of the era, during the Roaring Twenties common stocks occupied a cultural position remarkably similar to Bitcoin (and arguably the S&P) today—they were viewed as the revolutionary investment of their era, and there was widespread belief that supply of stocks was too scarce to meet surging demand.

In the 1920s, mutual funds were introduced under the name “investment trusts,” and—like Bitcoin treasury companies—formed to capitalize on this scarcity. A major difference between modern mutual funds and these trusts was that the trusts were leveraged: like Bitcoin treasuries, they invested using borrowed money that was considered “safe” because—like MicroStrategy—they issued preferreds and long-term debt securities to the public to buy portfolios of stocks. Galbraith:

The most notable piece of speculative architecture of the late twenties, and the one by which, more than any other device, the public demand for common stocks was satisfied, was the investment trust. The investment trust did not promote new enterprises or enlarge old ones. It merely arranged that people could own stock in old companies through the medium of new ones.

Democratizing Access to the "Next Big Thing"

Both the 1920s investment trusts and today's Bitcoin treasury companies emerged to “democratize” access to exciting, scarce assets that ordinary investors found intimidating or complex. In the 1920s, Wall Street was widely perceived as a "rigged game" dominated by ultra-wealthy insiders with monopolized information.

Investment trusts promised to level the playing field for the flood of new middle-class investors entering the market, by offering professional management, instant diversification, and simple access to the bull market through a single purchase. Even Keynes delegated his U.S. stock investing to professional trust managers, recognizing their superior grasp of American markets, while continuing to manage U.K. stocks himself.

Bitcoin treasury companies offer a strikingly similar value proposition today. While anyone can buy Bitcoin directly and custody it themselves, doing so requires navigating crypto exchanges, managing digital wallets, and securing private keys—a learning curve many traditional investors find daunting or impossible due to regulatory constraints.

Companies like MicroStrategy provide familiar regulatory wrappers that allow investors to gain Bitcoin exposure through ordinary stock purchases in their existing brokerage accounts. Investors are also buying into the perceived expertise of leaders like Michael Saylor, trusting them to handle the complexities of acquiring and storing large Bitcoin positions—and presumably later deploying capital wisely post-"HyperBitcoinization.”

mNAV During the 1920s

Like Bitcoin Treasuries, the 1920s trusts had the added appeal of mNAV premiums that seemed to offer something for nothing.

Just as Bitcoin treasury companies today boast of their mNAV and 'bitcoin yield,' a key feature of the 1920s bubble was the tendency for investment trusts to trade at significant premiums to mNAV during their heyday. Galbraith:

The measure of this respect for financial genius was the relation of the market value of the outstanding securities of the investment trusts to the value of the securities they owned.

Normally, the securities of the trust were worth considerably more than the property it owned—sometimes even twice as much. There should be no ambiguity on this point: the only property of the investment trust was the common and preferred stocks, debentures, mortgages, bonds, and cash that it held. (Often, it had neither an office nor office furniture; the sponsoring firm ran the investment trust out of its own quarters.)

Yet, had these securities all been sold on the market, the proceeds would invariably have been less—and often much less—than the current value of the outstanding securities of the investment company. The latter, obviously, had some claim to value that went well beyond the assets behind them.

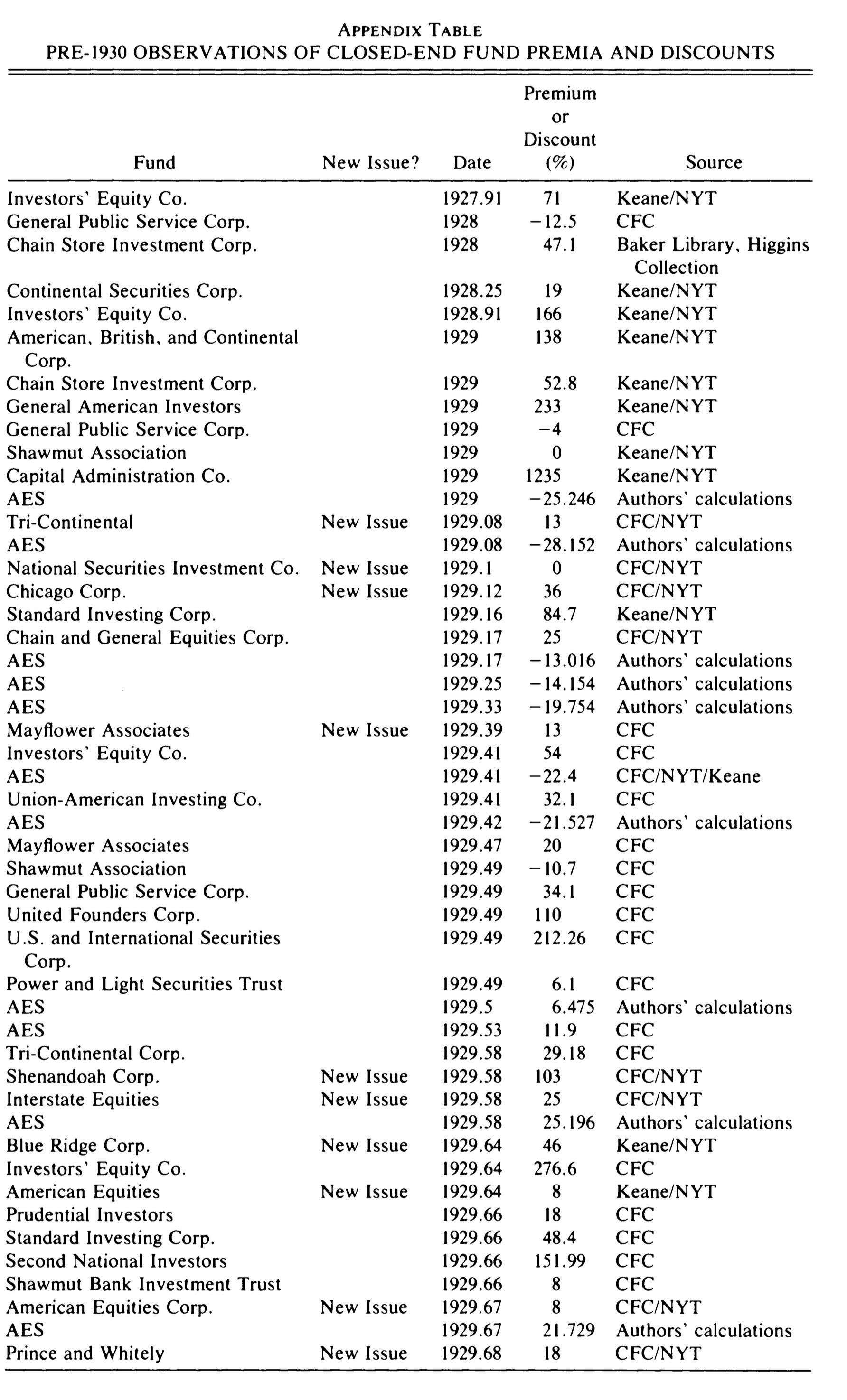

The Magazine of Wall Street recommended the following guidelines for selecting trusts on September 21, 1929.

Shares of an investment company capitalized with common stock only and earning 10 percent net on invested capital might be fairly priced at 40 percent to 50 percent in excess of share liquidating value [mNAV]. If the past record of management indicates that it can average 20 percent or more on its funds, a price of 150 percent to 200 percent above liquidating value might be reasonable.... To evaluate an investment trust common stock, preceded by bonds or preferred stock, a simple rule is to add 30 percent to 100 percent, or more, depending upon one's estimateof the management's worth, to the liquidating value of the investment company's total assets.

As Brad DeLong/Shleifer noted about this so-called investment “advice”:

This recommendation, made only a month before the Great Crash, assumes as a matter of course that funds should be selling at large premia; managers' ability to pick stocks is thought to multiply the value of the fund by a factor ranging from 3/2 to 3. Moreover, investors are advised to chase the trend—to load up on funds whose assets have shown good performance in the past—on the theory that their managers are the best.

The paragraph just quoted would seem eccentric in the post–World War II period, when funds have typically sold at discounts.

Investment analysts trying to direct investors away from closed-end mutual funds also wrote as if such funds sold at far above net asset value in the third quarter of 1929 and earlier. McNeel's Financial Service in Boston, for example, ran a series of large advertisements in 1929 issues of Commerce and Finance, asking (in bold type), "Are You Paying $800 for General Electric When You Buy Investment Trusts?"

These advertisements noted that investment trust stocks were "in many instances selling for two or three times... asset value. They are issued to the public and almost immediately quoted double or treble the issue price."

mNAV Magic

As with today’s Bitcoin TreasuryCos, this persistent mNAV premium created a powerful financial engine for both the trusts and the underlying stocks they were buying: the ability to conduct immediately accretive share issuances. When a trust trades at a premium to its underlying stock values, it can issue new units at the inflated market price and instantly increase the NAV for its existing shareholders.

This reflexive accretion mechanism created a self-reinforcing feedback loop similar to today’s "Bitcoin Leverage Loop". The cycle worked as follows:

Investor optimism drove a trust's price to an mNAV premium.

The trust would issue new units at this premium price, which was immediately accretive to the NAV per share.

The new capital raised was used to purchase more stocks, adding buying pressure to the overall market and increasing the value of the trust's own portfolio.

The rising NAV and apparent success of the strategy further fueled investor optimism, widening the premium and allowing the cycle to repeat.

Meanwhile, investors in the trusts and individual stocks amplified their exposure to a sure thing by using margin loans to leverage their positions, adding extra "juice" to the trade and further driving up NAVs and mNAVs for the trusts.

Galbraith noted that this mNAV process allowed trusts to create "an almost complete divorce of the volume of corporate securities outstanding from the volume of [undelrying] corporate assets in existence," as they could create a virtually infinite supply of their own shares to meet the public's insatiable demand. This dynamic was a core driver of the bubble's inflation and a key point of systemic fragility that would later prove catastrophic in the crash.

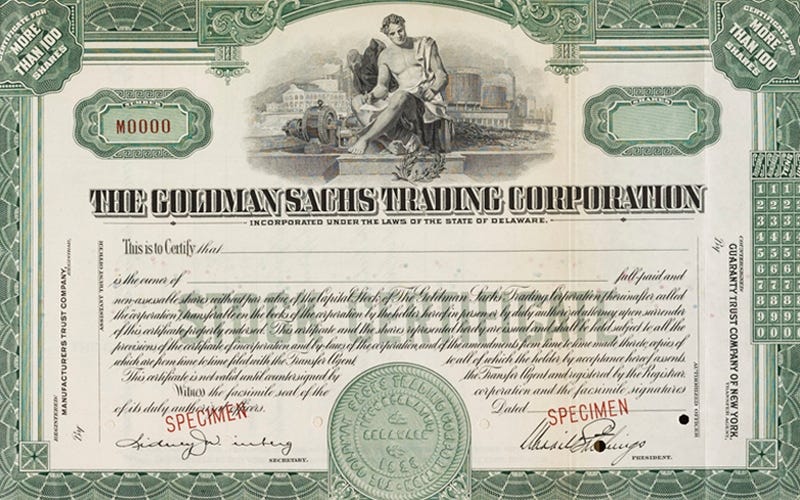

Goldman Sachs Trading Corporation As Proto-BTC TreasuryCo

Goldman Sachs Trading Corporation (GSTC) was perhaps the proto-MicroStrategy of the day. Launched by the influential Goldman Sachs partner Waddill Catchings in December 1928, it was, at its inception, the largest investment trust yet established—boasting an initial capitalization of $100 million. Its units, offered to the public at $104, was immediately oversubscribed and quickly soared in value, doubling to $226 within a short period and trading at a massive premium to the underlying value of its stock holdings.

Pyramiding Trusts

The initial success of GSTC was not enough for Catchings. To further amplify returns and absorb the public's insatiable demand for “scarce” stocks, Goldman Sachs constructed a pyramid of investment trusts. This "trusts within a trust" pyramid structure was designed for maximum leverage, meaning that a small rise (or drop) in stock prices could trigger significant gains (or losses).

In Brad DeLong and Andrei Shleifer’s The Stock Market Bubble of 1929: Evidence from Closed-end Mutual Funds, they noted:

If [investment trust mNAV premia] indeed reflect excessive investor optimism rather than skill at management, there will be a tendency for funds to pyramid on top of one another. If each fund can be sold for 50 percent more than its own net asset value, promoters can more than double their profits by establishing a fund that owns funds that hold stocks, rather than just establishing funds that hold stocks…

This prediction is confirmed by one of the largest funds: the Goldman Sachs Trading Corporation. This was a closed-end fund organized in December 1928 with a net asset value of around $100 million. In 1929, one of its largest holdings was the Shenandoah Corporation, another closed-end fund organized by Goldman Sachs. Another large holding was in its own stock.

Nor is this all. In the same year, Shenandoah organized a new closed-end fund called the Blue Ridge Corporation and became a large investor in its stock. All these funds traded at premia; at the top of the pyramid, the Goldman Sachs Trading Corporation traded at a premium to a premium to a premium to net asset value.

It is hard to justify these pyramided financial structures as anything other than an attempt to part fools from their money by capitalizing on layer upon layer of investor overvaluation. Goldman Sachs’s attempts to satisfy its customers’ demands for “funds that hold funds” and “funds that hold funds that hold funds” suggested to Galbraith that it was “difficult not to marvel at the imagination which was implicit in this gigantic insanity. If there must be madness something may be said for having it on a heroic scale.”

If history serves as any guide, we can expect Bitcoin treasury companies to begin investing in other Bitcoin treasury companies before this cycle concludes. Anyone familiar with the toxic confluence of YOLO-style investor behavior, passive investing, and algorithmic tradebots that has taken root since the QE era—the very behaviors we’ve been documenting in The Sorcerer’s Apprentice—should mentally prepare themselves for speculative excesses in Bitcoin and Bitcoin TreasuryCos that could reach levels far beyond what any reasonable person would consider sane before these leveraged vehicles collapse. Should any TreasuryCo or ambitious banker reading this choose to pursue such a pyramiding strategy, we trust they’ll remember to send along our consulting fee and royalty checks.

Exchange Of Assets

It’s worth noting another parallel with Bitcoin Trusts. When Goldman’s Blue Ridge Corporation was launched on August 20, 1929, it offered investors two ways to acquire its shares. The first was a traditional cash purchase. The second, more innovative method was a direct exchange of stock. This allowed an investor who already owned shares in certain established, blue-chip companies to trade them directly for a combination of Blue Ridge's own common and preferred stock.

This removed the friction of having to sell one's existing holdings, wait for the cash to settle, and then use that cash to buy into the new trust. It was a seamless, one-transaction process designed for maximum convenience. We see similar innovations in Bitcoin Treasury companies today, such as Strive’s clever Bitcoin exchange cum tax arbitrage:

The combined company will be the first to offer an exchange of Bitcoin for public company equity in a transaction intended to be tax-free to investors under section 351 of the U.S. tax code.

Up Next: Part III

The echoes between today's Bitcoin treasury mania and the investment trust bubble of the 1920s are too striking to dismiss. Both epochs feature the same intoxicating cocktail of scarce assets, leveraged financial engineering, mNAV premiums that seem to conjure value from thin air, and the seductive promise of democratizing access to revolutionary investments.

In Part III, we'll examine how the 1929 crash unfolded for these leveraged investment vehicles and consider whether Bitcoin's unique properties might save today's treasury companies from repeating financial history's most expensive lessons.

Thank you for this well-written and insightful post.

Thank you for this! Very interesting history lesson - and very applicable to the present in a time where companies get nav premiums just for the announcement that they will issue debt to buy bitcoin - before even issuing the debt at all let alone buying bitcoin