Metastasizing Monetary Mirage

Symbolic Alchemy Of Risk Part II: The Tower Of Babel

From Versailles To The Eccles Building

No experience or sufferings can cure the world of its [gullibility]. It has been a bubble from the beginning; nor [are people any] wiser for this discovery, but still [run] into old snares [when they are disguised by] new names, and often [even when they’re not disguised at all].

Self-love beguiles men into false hopes…[of gaining wealth] advantages which are purely imaginary, and utterly impossible.

—Cato’s Letters, No. 6, December 10, 1720, on the South Sea Bubble

In Part I, we explored how John Law pioneered the first systematic experiment in financial alchemy. Law's experiment collapsed spectacularly, but the ideas behind it survived and metastasized. As John T. Flynn observed nearly a hundred years ago: "If you would see [John Law’s] monument, look about you."

What Law pioneered through crude paper instruments at Versailles, our modern Sorcerer’s Apprentices have perfected with digital precision and automation on a civilizational scale from the Fed’s Eccles Building. They’ve embedded Law’s alchemy into the foundational architecture of global 21st-century finance, giving birth to the Financial Matrix—markets that function like a videogame simulation.

This journey through financial alchemy's evolution will reveal the 2008 Crisis not as a “black swan” or a one-off “market failure” caused by a few years of subprime and CDO excesses, but rather as the inevitable culmination of decades spent perfecting the dark art of risk transmutation. More troubling still, our alchemists have doubled down on these same transmutational principles since 2008—constructing an ever more elaborate apparatus for obscuring systemic fragility while amplifying it to scales that dwarf the leadup to the 2008 crisis.

Receive our latest insights on X/Twitter here. Suggestions? feedback@bewaterltd.com

Not investment advice. For educational/informational purposes only. See Disclaimer.

The following was originally published privately on January 13, 2021. Updated, revised, and expanded for public release on June 28, 2025. New to the Sorcerer’s Apprentice series? For essential context, start with our foundational chapters on the Financial Matrix, Hyperreality, and The Flight Into Fake Values, or explore the full Table Of Contents.

Ten Milestones On The Road To Hyperreality

1. The Metamorphosis Of Money

2. Keynes' Kaleidoscope

3. Money Printer Go BRRRR

4. Silicon Shadows

5. The Rise of Skynet

6. The Institutionalization Of Finance

7. The Symbolic Alchemy Of Risk <== YOU ARE HERE

8. “We’re All Quants Now”

9. Social Media, Memes, & Machines

10. The Consumerification of FinanceThe Deluded Speculators’ Tower of Babel (1720)

The engraving below—created in the aftermath of Law's experiment—eerily prefigures the 2008 crisis and today's even more precarious system:

The Great Mirror of Folly’s Tower Of Babel shows financial alchemy's grotesque endpoint: speculators suffer from diarrhea after gorging on “stock cakes”—a metaphor for dubious, fraudulent, or inflated financial products—and use their now-worthless certificates as toilet paper. John Law is seated on the bottom left, actively issuing and signing shares; the Tower of Babel rises in the background, symbolizing the hubris of this alchemical endeavor.

On the right side, a vendor—likely a personification of English financial fraud, and possibly representing Sir John Blunt—cooks deceptive stock cakes labeled ‘Smoke,’ ‘Wind,’ ‘Bad Shares,’ and ‘English Shares’. While some interpretations identify this figure as John Law, the labeling suggests a stronger alignment with the South Sea Bubble and English speculation, making Blunt the more likely symbolic target.

Above the chaos, Fortune—a blindfolded woman—rises from smoke while Wisdom exposes Fraud by pulling away her dress to reveal clawed feet. Financial predation is symbolized by a hawk killing a smaller bird, while a ruined investor throws himself from a window in despair.

The banner at the top reads:

Greed drives many souls to ruin chasing profit,

Who, blinded by love of illusory wealth,

Lose their work, clothes, and even their very status.

All is lost. Let those drowning in debt take warning:

What they found in shares was mere air and wind—

Empty shadows, never touched by substance.

Below the scene is a poem in four columns (our full translation here):

Behold how Law's grand scheme collapsed—

His paper empire turned to ash.

While foolish stocks like hotcakes sold,

Men fought for shares with dreams of gold.

They soiled themselves in frantic greed,

Then found their papers served a need:

To wipe their backsides, raw and red,

With shares once prized, now worthless instead...

Moral

Like Babel's tower, built with pride,

They fell beneath the stars they eyed.

The people, filled with rage and shame,

Repent this madness and its blame.

Let this example warn posterity—

This alchemy was the utmost folly,

So let this madness stand in fame—

A monument to Babel’s shame.

Today we have erected our own global investment Tower of Babel, ascending to heights far grander than anything Law or Flynn could imagine. Our modern Tower was built upon four foundational layers: first, money itself had to be transmuted from substance to symbol. Then government debt had to become 'risk-free.' Next, housing and mortgages had to be transformed into liquid, nearly ‘risk-free’ investments as well. Finally, all of this risk to be packaged into money-like instruments that could circulate globally.

Each layer enabled the next—and led inexorably to the 2008 collapse. Since the Crisis, our alchemists have stacked additional layers on top, constructing the Financial Matrix—an even more precarious system that we'll examine in the next chapter.

Metamorphosis Of Money: From Substance To Symbol

Our alchemists began by transmuting money from substance to symbol, declaring that money is whatever the State says it is and replacing a tangible asset with paper debt—IOUs from the Federal Reserve system.

For the first time in history, all of civilization became enmeshed in a kaleidoscopic, self-referential global monetary system. The severance of money from physical reality laid the foundation for our Tower Of Babel, creating the necessary precondition for every subsequent alchemical experiment, and initiated our modern age of financial sorcery.

Transmuting Treasuries: The Spreading Enchantment

Having severed money from physical reality in 1971, the alchemists faced their next challenge: extending their transmutation powers beyond currency itself to the broader universe of financial assets. They needed a proof of concept—a demonstration that they could weave a spell over any instrument they chose to enchant.

The alchemists turned to US Treasury bonds—the type of government IOUs that throughout history had regularly defaulted, leaving investors wiped out through debasement and repudiation (including at least three episodes in U.S. history that arguably qualify as technical defaults). Through academic theorizing, regulatory embedding, and the global demand created by dollar reserve currency effects, the alchemists achieved something that would have made John Law weep with envy: they entranced the entire world into believing that these government promises had been symbolically transformed from risky IOUs into "The Risk-Free Rate."

Not content with creating money from nothing, our alchemists had now created safety from risk, certainty from uncertainty. The very meme "Risk-Free Rate" became the foundational axiom of Modern Finance, embedded so deeply in orthodoxy that questioning it became almost unthinkable.

By the 1990s, regulatory bodies and institutions had woven Treasury-based calculations into the fabric of banking, investing, and financial ‘compliance’. Basel banking accords granted Treasuries privileged status—giving banks an incentive to load up on government debt versus other more productive assets. Until relatively recently, ratings agencies consecrated Treasuries with the highest possible rating—AAA.

Treasuries began to function as the baseline against which all other risks and returns are measured. The "Risk-Free Rate" became the gravitational center around which all other financial assets would orbit, serving as the base input for everything from the Capital Asset Pricing Model (CAPM) to Modern Portfolio Theory (MPT) to options pricing formulas.

This wasn't merely an academic exercise—this single meme became the foundational fiction supporting global financial alchemy. An entire civilization now priced assets and measured risk based on the ahistorical premise that a government—specifically the US government—never defaults.

But the transmutation of Treasuries served a far more important purpose than merely creating an illusion of safety that allowed the government to borrow more cheaply than it otherwise would. It established the methodology that would later be applied to subsequent alchemical experiments: symbolic transmutation, academic legitimization, regulatory capture, institutional embedding—backstopped by central banks—could memetically transform any asset into whatever symbol the alchemists needed it to become.

The Alchemy Of Housing

The alchemists’ next target emerged out of necessity. After their Dotcom bubble crashed in 2000, central bankers were left scrambling for a replacement bubble to paper over the wreckage they themselves had created. They needed an asset that was far more pervasive than tech stocks—a market that could absorb massive leverage while touching every American household:

2008’s Deeper Roots: Government Sponsored Mortgage Alchemy

Conveniently, all the infrastructure required to inflate this bubble had already been in place for decades—and indeed had already been inflating housing prior to the subprime boom. The roots of the financial crisis extend far deeper than the subprime lending and Collateralized Debt Obligation (CDO) boom that dominated headlines.

The true foundation was laid during FDR’s New Deal, in response to the Great Depression. Like the 2008 crisis, the Fed’s reckless monetary policies during the “Roaring Twenties” helped fuel a speculative stock bubble cthat burst in 1929, triggering widespread economic collapse. By 1933, a quarter of all American homeowners had lost their homes in the resulting Great Depression.

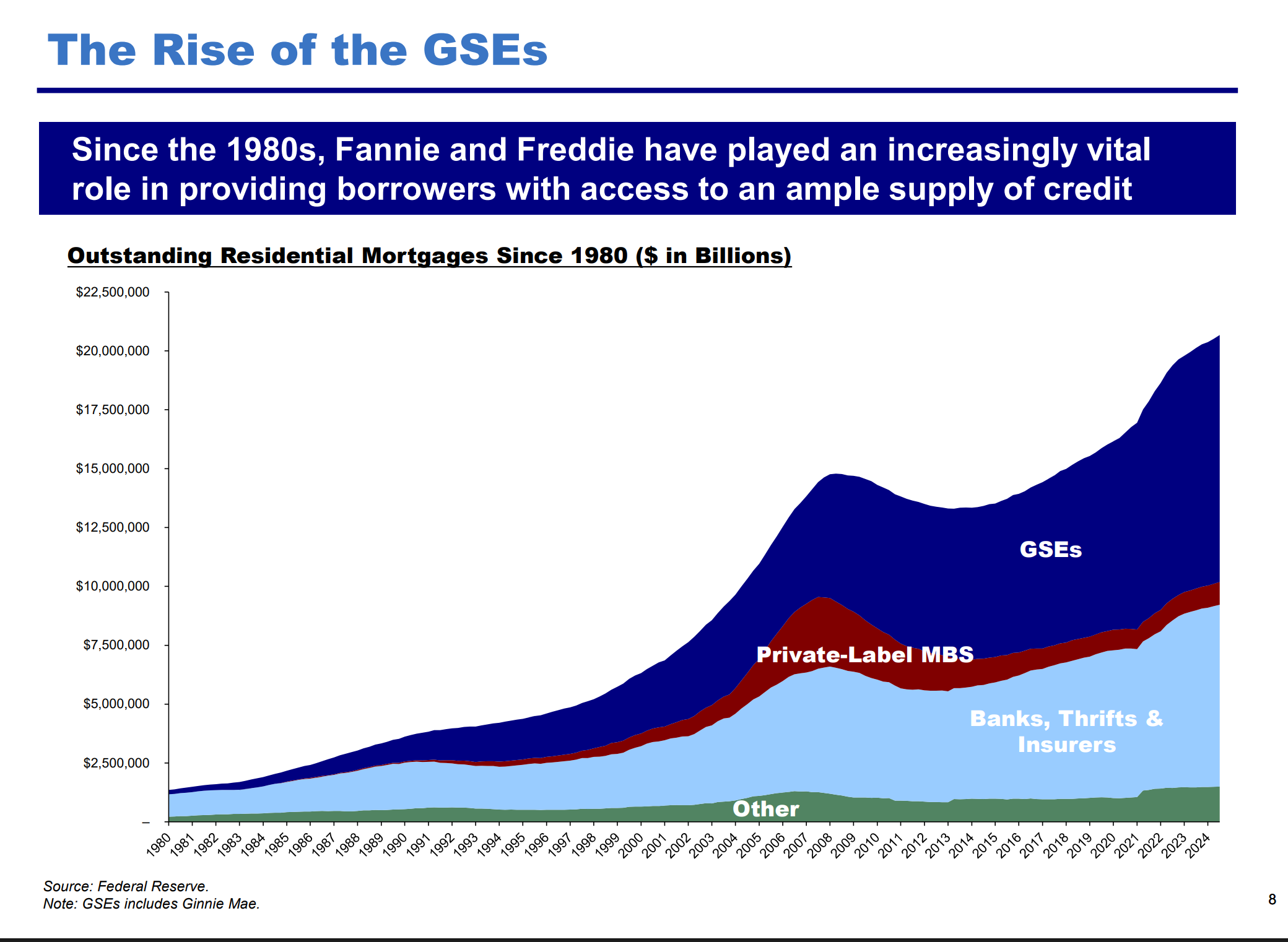

After his reverse alchemy turned money from gold into paper, FDR applied the same symbolic alchemy to housing—establishing the precedent that homes deserved continuous government support as a cornerstone of economic policy. The New Deal created Fannie Mae in 1938 as one of the first major Government Sponsored Enterprises (GSEs) that would come to reshape American housing finance.

The GSEs and the mortgages they touched came to be seen as nearly as safe as Treasuries. The alchemical logic was elegant: because government bonds were risk-free, a mortgage (implicitly) backed by the government also became (nearly) risk-free, creating a transitive property of safety.

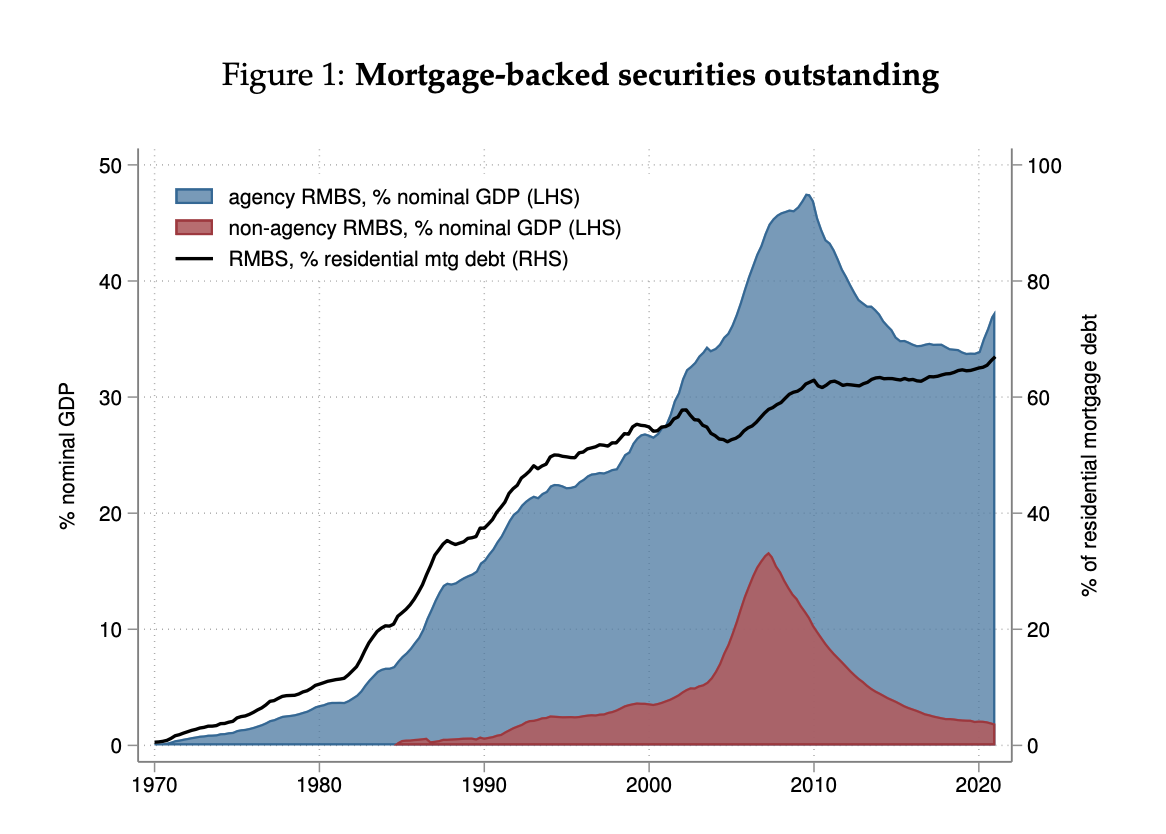

Fannie transitioned from a government agency to private shareholder ownership in 1968. Two years later, Congress created Freddie Mac to provide competition to Fannie and additional liquidity to the secondary mortgage market. Not long after the Nixon Shock finished off what had remained of the gold standard in 1971, Freddie issued its first mortgage-backed securities (MBS); Fannie followed suit in 1981.

The GSEs purchased mortgages from lenders and packaged them into MBS, freeing up capital at the banks, enabling banks and other loan originators to issue far more housing loans than were previously possible. Securitization allowed Wall Street to sell mortgages to investors as a virtually “risk free” commodity at enormous scale due to the implicit government guarantee of the GSEs. This alchemy of housing risk translated directly into easier access to loans and lower mortgage rates for borrowers, which in turn artificially inflated housing demand—and therefore prices—by increasing buyers’ purchasing power relative to their salaries.

Both GSEs expanded operations dramatically in the 1980s and began to standardize the securitization process. This connected home lending to global capital markets, vastly increasing the supply of mortgage funding; a hedge fund or foreign investor might now own your mortgage rather than your local banker.

The MBS market turned the incentive structure of mortgage lending on its head. By creating a liquid secondary mortgage market for the first time, lenders could now make loans and immediately sell them rather than being forced to hold them long-term, severing the connection between those making loans and those taking the risk the loan might not be paid back. Profits were now tied to loan volume rather than loan quality, and underwriting standards began to deteriorate as there was less “skin in the game”—the profits were privatized, but any losses were socialized thanks to the government backing.

This alchemy fundamentally transformed the housing market. What had traditionally been a local, relationship-based market rooted in community banks' intimate knowledge of their borrowers became a national commodity. Government backing of mortgages and Wall Street’s MBS machine flooded the market with virtually unlimited cheap credit.

In particular, following the collapse of the Northeast and California real estate bubbles in 1991—during the most precarious period for banks and S&Ls—Fannie Mae and Freddie Mac began to aggressively expand their balance sheets in an apparent attempt to paper over those crises.

The GSE’s enabled gold to be fabricated from drywall and debt—transforming the American Dream into the raw material for financial elixirs sold the world over, as Margot Robbie memorably explained in The Big Short:

The Great Symbolic Inversion: From Shelter to Speculation

By the time Paul Krugman recommended that Greenspan’s Fed inflate a housing bubble in 2001-2002, therefore, Fannie and Freddie had already spent decades perfecting the transmutation of mortgage risk into “safe” securities. The Fed and GSEs’ implicit backing of mortgage credit had radically altered market risk perceptions for housing and mortgages beginning as far back as the 1980s.

The profitability of this arrangement was evident early on: Peter Lynch famously declared Fannie Mae "the best business, literally, in America" in 1986, marveling that the company employed a quarter of Fidelity's workforce while generating ten times the profits. Financial alchemy, it turned out, was remarkably lucrative.

As result of the GSEs, houses and mortgage debt were symbolically transformed into “safe asset classes” unto themselves. Operating as shadow quasi-central banks alongside the Federal Reserve, Fannie and Freddie quietly fueled the nationwide—and arguably global—housing bubble that emerged in the 1980s and gained momentum throughout the 1990s.

In the process, the GSEs created the template that private markets would later amplify through increasingly exotic instruments during the subprime securitization boom of the early 2000s, including the mathematical models, market-making infrastructure, and “credit enhancement” mechanisms—such as guarantees against mortgage default implicitly backed by the U.S. government.

The methodology mirrored the alchemists’ Treasury playbook: symbolic transmutation, academic/mathematical models replaced economic reality, regulatory blessing replaced market discipline, and ratings agencies sanctified the alchemical process for fees.

Basel Accords again provided a spellbook, treating mortgage debt preferentially and creating another profound distortion in banking incentives: financing suburban real estate speculation became more profitable than lending to businesses actually creating goods and services. Ratings agencies again sanctified the alchemical process for fees, stamping "AAA" ratings on securities backed by risky mortgages.

Other countries such as Sweden, Canada, and Australia adopted similar alchemical playbooks to support their own housing markets, and the “moneyness” of housing and mortgage debt attracted global capital flows. As a result, the middle class across the globe was drawn into a game of asset inflation or stagnation—buy now or forever be left behind.

Wall Street reveled in its ability to alchemically convert an endless torrent of risky mortgage loans into perceived safe and liquid securities through a daisy-chain of explicit and implicit guarantees—GSE backing, credit insurance, liquidity agreements, and an expansive derivatives marketplace—all ultimately supported by faith in the Fed and Treasury.

Evolving insidiously over time, this alchemical liquidity helped fuel successive leveraged bubbles—including tech stocks in the 1990s, and later housing and consumption in the 2000s.

Fannie and Freddie were the hidden architects behind the transformation of homes and mortgages into the world’s most important (and leveragable) speculative commodity. What appeared to be genuine prosperity was John Law-inspired alchemy masquerading as economic growth, making collapse inevitable once the liquidity slowed in 2007-2008. Even without the added fuel of subprime lending and CDOs, this system would have eventually collapsed under its own contradictions.

The Symbolic Alchemy Of CrediCash

Meanwhile, demand exploded for debt issued by Fannie and Freddie themselves; this so-called agency debt was issued to fund their mortgage purchases and the mortgage-backed securities they created. There was insatiable demand for these IOUs; agency debt, mortgages, and MBS became core holdings throughout the global financial system, including in cash management and “money market” funds.

This created what we call CrediCash—a highly liquid, “safe” instrument that circulates as if it were money due to perceived liquidity and government guarantees. The agencies were able to issue virtually unlimited quantities of new IOUs—agency debt and mortgage-backed securities— with no deleterious impact on the market’s perception of their money-like status because of their implicit government backing.

Our alchemists wove this disguised housing risk into the very fabric of the global monetary system; speculators then used CrediCash to cheaply fund real estate and other asset market bets globally. Investors believed they can get their “money” out anytime—until the moment that trust evaporates, the underlying risks are exposed, and the whole system seizes up.

The 1990s were the heyday of check-writing from Money Market Funds (MMFs) and “sweep accounts”, both of which reinforced the illusion that credit was as liquid and risk-free as cash. These MMFs grew into massive funding vehicles; a large share of their assets was invested in short-term debt issued by GSE-related debt and mortgages, effectively channeling trillions into the housing market. This created a powerful feedback loop: sweep accounts fed MMFs, MMFs funded GSEs, and GSEs pumped credit into housing—driving up home prices and spurring even more borrowing.

The easy flow of credit extended far beyond housing markets. Rising home values bolstered consumer confidence and provided additional collateral, which fueled increased consumption and stock market investment. Simultaneously, low interest rates and abundant liquidity drove investors to seek higher returns, inflating stock prices in tandem with real estate values. The seemingly limitless profit potential in these markets ensured that both real and financial assets captured the vast majority of available lending and finance. In this environment, the finite universe of productive investment opportunities struggled to compete for lender attention against the allure of appreciating—and increasingly inflated—asset markets.

2008 Was Not A Subprime Crisis

Thanks to popular media accounts of the crisis such as the Big Short, the public focuses on esoteric instruments such as subprime and CDOs. This obscures the deeper alchemical process that took place, as these now-infamous instruments were merely the most visible symptoms of a systematic symbolic inversion that began with Money’s Metamorphosis and Treasuries’ Transmutation.

The fixation on these specific mechanisms also blinds observers to similar alchemical processes in other assets and geographies that don't exhibit the particular American pathologies of 2002-2006. For example, it creates a false sense of immunity regarding the arguably worse housing bubbles in markets like Sweden, Australia and Canada, where the same fundamental alchemical processes unfold through different instruments, channels, and institutional contexts.

The Great Financial Crisis was not primarily the result of new derivatives, a few reckless lenders, or regulatory failure as the conventional narrative suggests. The crisis was the inevitable consequence of a broken monetary system and the systematic alchemical transformation of government debt, housing, and mortgages.

The spell worked exactly as Paul Krugman and other economists intended—channeling trillions of dollars into speculative bidding wars over condos and suburban real estate in order to “replace the Nasdaq bubble” with an even bigger housing bubble. The Crisis was the result of a generalized credit bubble, not simply a subprime bubble; the result of the credit bubble was a feedback loop wherein credit creation drove asset inflation, and inflated assets justified more credit—pushing both housing and equities into twin bubbles. When reality finally reasserted itself, the transmutation briefly reversed with devastating speed—before our alchemists again doubled down on alchemy to paper over the crisis.

Up Next: Part III, The Everything Bubble

John Law proved that paper could temporarily become gold through State backing and mass memetic conviction. Today's alchemists have erected Law's vision on such a scale that the entire world must participate in the experiment—whether they choose to or not.